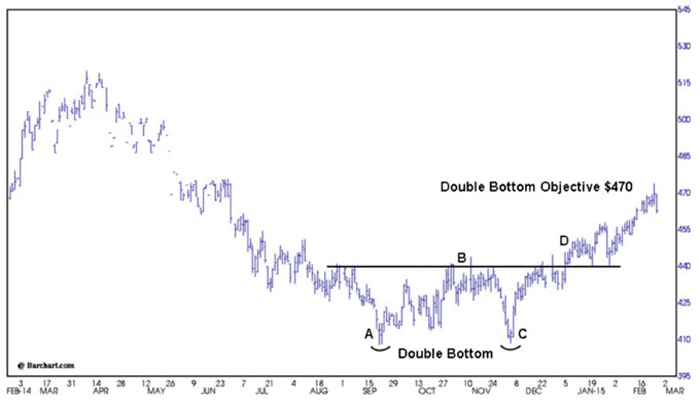

Canola has rallied $65 per tonne since Dec. 4, 2014, the day the May 2015 futures contract turned up from a second low at $408.60. A chart pattern known as a double bottom indicated the May futures contract would rally to $470 per tonne, a level not seen since June 30, 2014.

Double bottom

Double bottoms are basic formations which appear with regularity in the futures markets. Once completed they are a reliable signal of a reversal of trend. A double bottom begins to take shape with prices advancing into new low ground for the current move. This low is illustrated as point (A) in the accompanying chart. A reaction then sets in during which a portion of the decline is retraced (B).

Read Also

Double cropping trial targets cattle feed boost in Alberta’s irrigation belt

A new five-year Farming Smarter study is testing double cropping systems for cattle feed production under irrigation in southern Alberta.

A second drop (C), brings prices back down to approximately the lows of the first decline. This is followed by a price rally (D), which exceeds the reaction high (B).

Time-wise, it is important that the two lows are not very close together. It should be three to five weeks or more. A time interval for completion measured in months would be indicative of a significant reversal of the major long-term trend.

Absolute price level need not be exact at the two bottoms. Often at a low, the second decline will slightly exceed the first low and appear very pronounced or spiked, but it may also fall shy of the first low.

In the double-bottom pattern, strong confirming evidence is to have high volume at both extreme low points, with the first low having higher volume than the second low.

The rally which follows the second bottom should see volume pick up. This pattern is completed when prices exceed the high between the two lows.

A minimum price objective is derived by measuring the distance between the reaction high (440) and the double bottom (410) and adding it to that high. Example: (440-410), (440+30G0).

Market psychology

The first low develops after a sustained price drop. It coincides with a growing willingness on the part of shorts with large unrealized profits to cash in their earnings.

The market stalls as the supply of contracts for sale is overwhelmed by short covering and prices begin to rise. Long buyers jump in, convinced that the downward move has gone far enough. The market continues to rally until the buyers withdraw. From a longer-term perspective the major trend is still down, so when the rally falters, sellers once again step in and prices begin to move lower.

At approximately the level of the first low, the shorts who failed to take profits when prices made the first low and sat through the entire correction are likely to be watching more closely and won’t let the opportunity to cash in slip so easily through their fingers the second time around. The decline is also halted by the ever-present bottom pickers who are waiting to buy the proverbial bottom of the market.

At the second low, the buying eclipses whatever selling remains and the market begins to gain ground.

When prices penetrate the reaction high between the two bottoms, all recent shorts will have paper losses and will eventually be potential buyers. Once prices fail to have any sustainable decline, hope begins to wane and covering of short contracts becomes an inevitable reality. As prices continue to rally, new longs will also enter the market.

Canola producers who keep a watchful eye on charting and technical analysis were alerted to the potential rally to $470 on the May futures contract. Technical measurements derived from chart patterns such as double bottoms and rectangular patterns often provide farmers with key price objectives.