What’s the basis for your basis decisions? Basis pricing doesn’t get as much attention as it should but is such an important, but often overlooked or misunderstood, piece of the grain-marketing puzzle.

While many farmers do pay close attention to basis, others don’t. I initially looked at basis in this column a couple of years ago and since it can have a big impact on your final cash price, it’s worthwhile revisiting it again.

As a refresher, basis is just the difference between your local cash price and the futures price. So, for cash markets like canola, wheat, corn and soybeans that have an associated futures market, their basis will be different all across the Prairies. Furthermore, the local basis level is often a negative number and reflects pricing differences between your cash commodity relative to the delivery specifications referenced in the futures contract including:

- Local supply-and-demand factors,

- Transportation and handling costs,

- Grade or quality differences, and

- Storage and carrying charges.

Basis and futures react to similar underlying trading factors including whether the market wants your grain now or in the future. Just as the velocity of money is an economic term used to describe how quickly money moves around the economy, basis levels can be thought of as an indication of the velocity of grain moving through the elevator pipeline system. When velocity is slow, grain stocks build and the basis price level decreases; when velocity picks up, grain stocks drop and the basis price level improves.

This grain velocity has its seasonal biases. Based on data and analysis from FARMCo., the relationship between primary elevator stocks and canola basis in the Par Region in central Saskatchewan shows a classic case of supply and demand. Over the course of the crop year from the beginning of August to the end of July, as canola elevator stocks build at harvest, basis reaches its lows coming in to September/October. It gradually improves as elevator stocks begin to decline near the beginning of November. From there, basis typically continues to climb as canola stocks dwindle until the next crop year when this process starts all over again.

While this basis behaviour can be quite persistent year after year, seasonal patterns are only tendencies and won’t necessarily work the same way every year. However, being aware of basis levels at different times of year can help improve your selling process. So far this year, canola basis levels have followed the typical seasonal pattern since last fall. When it comes to wheat, although Minneapolis futures are down about 10 per cent this year, CWRS cash bids across the Prairies are essentially unchanged this year thanks to a weak Canadian dollar and improving basis levels, as per the accompanying chart in C$/bushel courtesy of PDQinfo.ca.

Read Also

Tariffs, trade wars and the Iran conflict: How Prairie farmers can manage unprecedented volatility

Prairie farmers face unprecedented volatility but experts say smarter contracts, fertilizer planning and diversification can help.

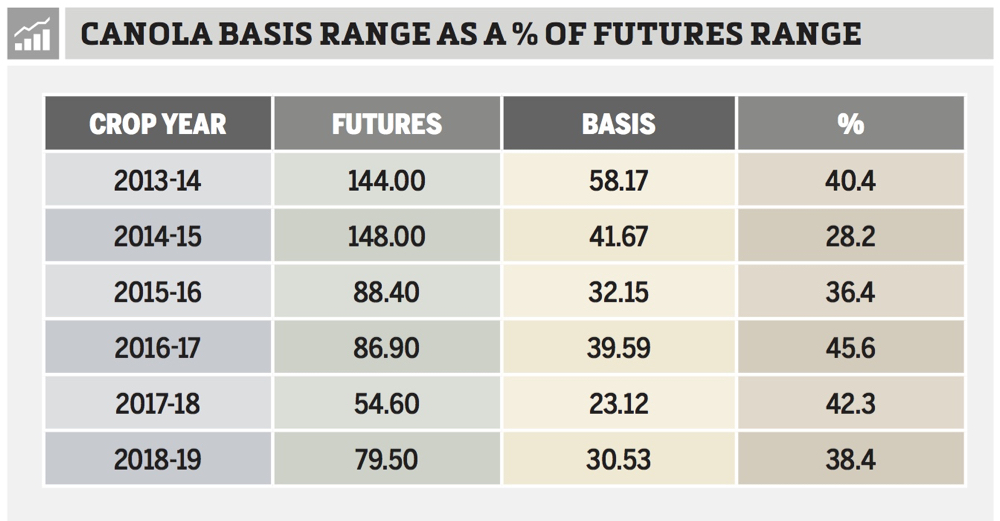

Not only does basis have its own seasonal pattern like many commodities, basis also has its own level of volatility. Once again using research from FARMCo., you can see that in the table called “Canola Basis Range as a % of Futures Range,” the overall top to bottom price range for canola futures varied from as much as $148/tonne to as little as $55/tonne, with an average of about $100/tonne in the past few years. Meanwhile, the canola basis range has been as high as $58/tonne to as low as $23/tonne, with an average of $38/tonne. Basis fluctuations have averaged 38 per cent of the underlying canola futures changes in the past few years meaning basis moves by over a third of outright futures prices. Clearly it’s worth paying attention to basis levels.

Bottom line, cash, basis, futures, delivery and storage are all pieces of the same marketing puzzle that work together to create the bigger picture. It makes dollars and sense to proactively track those trends and make those marketing decisions separately. Incorporating futures and options allows you to enhance your existing physical sales and basis decisions. If basis is strong but futures are weak, you can lock in the basis now and price the futures component later. Or, if futures prices are good, but basis is poor, hedge the price with futures now and then wait for basis to improve. This diversification of your grain revenue management strategies can help you capture extra returns and take your grain marketing to the next level.