It is definitely one conference not to be missed. Numerous speakers covered various topics although this year it seemed that most things that made me go “hmmm” were in the areas of trade dynamics, political/social factors, marketing and, of course, technology.

Political and social factors dominated many of the sessions with suggestions that there will be more geopolitical risks and opportunities going forward. Here are a few things to keep an eye on in this area.

One is Russia as it continues to expand its sphere of influence. This is nothing new given its previous activity in Crimea, Ukraine, Syria and other countries throughout South America and Asia.

Read Also

Manitoba cattle prices April 14

Here are the prices Manitoba beef and other cattle producers could expect to take home from the sale of their livestock April 8-14, 2026.

Another geopolitical factor is, of course, the continuing Chinese economic evolution. It was said that the recent U.S.-China trade wars should not be viewed as a short-term isolated event but rather a condition whereby the U.S. and China are locked into a long-term strategic trade competition. While China needs oil and food security, don’t base your farm’s future growth strategy on just China. Perhaps India will become the next China, since it too will likely be massive buyers of food. This would be a good development for Canadian farmers.

Another geopolitical issue was increasing American isolationism with the U.S. becoming more self-absorbed. This is being driven by the “Make America Great Again” presidency as well as U.S. oil independence and their petroleum product export expansion. This could mean less U.S. involvement globally, and, in particular, less influence in oil-producing countries.

Turning to demographics and population issues, while the massive rapid urbanization trend in the developing world will likely continue, population growth won’t necessarily. It was stated that only Africa will have population growth going forward. It was forecast that China will lose 300 million people by 2100 due to the declining birth rate. As a result, China may not be the global power we think it will be.

Overall, expect global population to top out at nine billion and then start to go down, contrary to the long-held Malthusian theory many people have subscribed to. Population decline, it was said, is good for the environment but bad for the economy.

This raised an interesting question: “How does capitalism work when population declines?” Economic growth rates always seem to be based on the consumption of more stuff, but if there aren’t more people, they won’t be buying more stuff.

Just look at Japan since its financial bubble burst in the late 1980s. Its aging population has been more or less sideways since the mid-1990s and at the same time, its economy, GDP and stock market haven’t gone anywhere for almost 30 years either.

A USDA Global Desertification Vulnerability Map was presented showing how areas in Africa, Eurasia, Russia, Australia, and even the U.S. are susceptible to drought and dry conditions. Some comments around this were that while North America has around eight per cent of the world’s population and 50 per cent of its water, Asia has 60 per cent of the population but only nine per cent of the water. This will cause a lot of issues, but a positive one could be more demand worldwide for our plentiful Canadian grain.

A statement made by one of the speakers that caught my attention was, as he put it, the most dangerous phrase in agriculture: “We’ve always done it this way.”

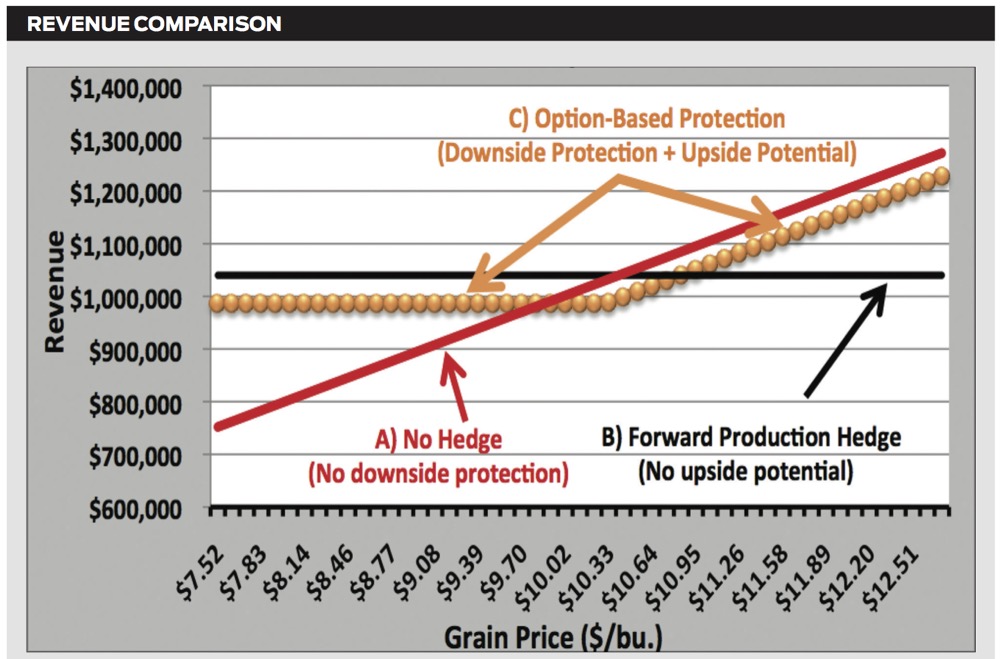

While this could apply to many areas of farming, it certainly applies to the world of marketing and hedging. While more and more farmers are using all the marketing tools available to them, there’s a lot more to go.

The speaker noted that two important areas to manage in farming are hedging policy risk and hedging currency movements. While it’s tough to hedge global or domestic politics, currencies are one way through which political risks are translated in to the markets and then converted into monetary form. I agree with his concern especially given that the Canadian dollar has been very quiet over the past few years and global interest rate policies are in a race to the bottom.

Another marketing-related point that was talked about is that there has not been enough pain from low corn, wheat and soybean prices yet to signal a change in what farmers will grow. Market prices will influence what producers grow by buying acres to encourage or discourage what gets put in to the ground. As always, watch commodity price trends.

Another recurring theme was the increasing diversity in the sourcing of grain input supplies. China, it was noted, has been importing soy and rapeseed meal from many new origins as of September 2019 while its use of palm and pea meal has been increasing recently as well.

These new commodity trading relationships have just been developed so they won’t unwind instantly if there is improvement in Canada-China trade relations. This means that canola prices won’t necessarily bounce back up automatically because Canada-China trade discussions improve.

Finally, we have technology factors. We all know of the many technological and scientific advances being made in agriculture but this one was surprising and very interesting.

Apparently an app that uses spectronomy is in development that can be used to assess wheat grade, quality, protein, moisture levels or to measure soil moisture content and other soil metrics. It’s supposed to be as easy as taking a picture. Regardless of whether this type of app ever makes it to market, technology is impacting the way farming gets done. Don’t be surprised about being surprised by the new ideas and products that emerge over the next several years.

Bottom line, farming and the commodity markets are constantly evolving so a conference like GrainWorld provides an edge for farmers who wear many hats. The advantage is combining all these ideas, data and information with our experience to better deal with new risks and opportunities on the farm.

Here’s to proactively looking ahead to the new crop year in 2020!