Canada exports almost a third of its gross domestic products of goods and services. And when it comes to agriculture, those percentages are even higher. Based on statistics from the Canadian Agri-Food Trade Alliance, we export 50 per cent of our beef/cattle, 65 per cent of our malt barley, 70 per cent of our soybeans, 70 per cent of our pork, 75 per cent of our wheat, 90 per cent of our canola and 95 per cent of our pulses. Canada has always been an exporting nation so a continuing low and stable Canadian dollar helps us compete in the global markets. But markets don’t always stay the same. They are constantly changing so you can’t expect this current environment to go on forever.

Read Also

Manitoba cattle prices April 14

Here are the prices Manitoba beef and other cattle producers could expect to take home from the sale of their livestock April 8-14, 2026.

While things may still remain status quo for months to come, any number of economic, political or financial factors could change current market conditions. For example, although most countries have relatively free floating currency policies, many economically significant countries like Saudi Arabia, Kuwait, Nigeria, China, Singapore and others have some level of long-standing currency peg against the U.S. dollar.

A change in their economies could cause those currencies to become unpegged and introduce a new element of volatility to the global foreign exchange market. Many of these countries are also petroleum-producing nations so any major changes to oil economics could also be a factor of change. Combined, these countries account for almost 20 per cent of global GDP so it’s not insignificant if some type of economic or political impact causes them to adjust their currency regimes.

Another potential trigger could be interest rates. Most countries have very low and falling interest rates. In fact, Japan and most countries in Europe have government bonds trading at negative interest rates. President Trump has been calling for negative central bank rates in the U.S. as well when he recently said: “Remember, we are actively competing with nations that openly cut interest rates so that many are now actually getting paid when they pay off their loan, known as negative interest. Give me some of that money.” Maybe this currency war race to the bottom will be the trigger that causes a change in market trends resulting in higher foreign exchange volatility.

And then, of course, there are the trade wars, which have been extensively covered very well elsewhere. It’s very hard to determine what impact this may have or when but it is still another issue that would influence currency movements.

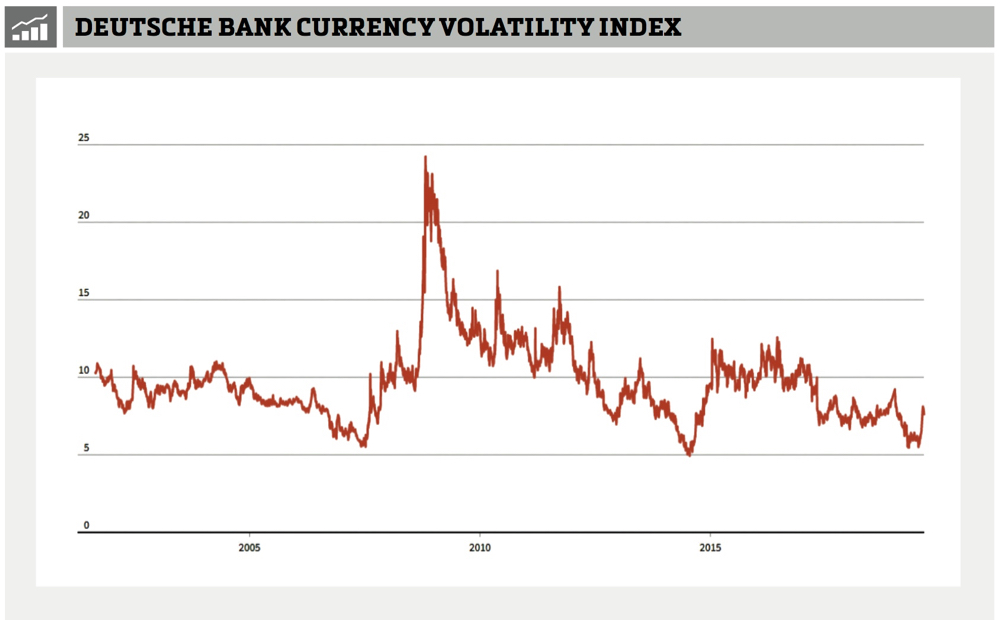

Regardless of what an eventual trigger might be, major currency markets have been quiet and relatively stable for the past couple of years. The Deutsche Bank Currency Volatility Index shows that global currency fluctuations have been near the low end of the range of the past 20 years (see below).

A period of low volatility in any market is often, but not always, followed by a period of expanding and higher volatility; sort of like the calm before the storm. When we look specifically at the Canadian/U.S. dollar chart, we can see similar patterns recurring over that past 20 years. After a prolonged time of quiet trading activity measured in months or even years, big movements in the C$, either up or down, often develop. We have witnessed stable conditions for over two years now. While it doesn’t mean that the loonie has to make a big move higher or lower, it does become more and more likely as time goes on.

Bottom line, the easy part is determining that Canadian dollar volatility has been quite low. The harder part is figuring out when that might change and what you’re going to do about it. As an exporter in the global commodity market, you want to capture as much of the benefit of a weak Canadian dollar as possible while still protecting against a strong C$.

In fact, the annual range of the C$ against the US$ can reach up to 10 per cent in any given year. That’s a lot of risk and opportunity. The trigger that shakes us out of the current low-volatility environment might be something we can’t even imagine right now or expect at this time. Alternatively, we may be in this same currency environment for many more months to come.

The most important question to ask yourself is: “What hedging strategies do I have in place to manage the currency impact on farm revenues?” The key is to start thinking about this now when the C$ is at 75 cents, near the low end of the range over the past 40 years, not if it’s at 95 cents. By then, it would be too late.