Canola futures found themselves under pressure to start the new 2025/26 (Aug/Jul) marketing year, with prices falling to their lowest levels in four months in the early days of August. Speculators liquidating long positions and spillover from a bearish tone in the Chicago soy complex accounted for much of the selling pressure, although the underlying fundamentals remain relatively supportive for the oilseed.

The full breakdown on the recently finished marketing year won’t be available until September, when Statistics Canada releases July export data and ending stocks numbers. However, the June export report released Aug. 5 paints an interesting picture for canola.

Read Also

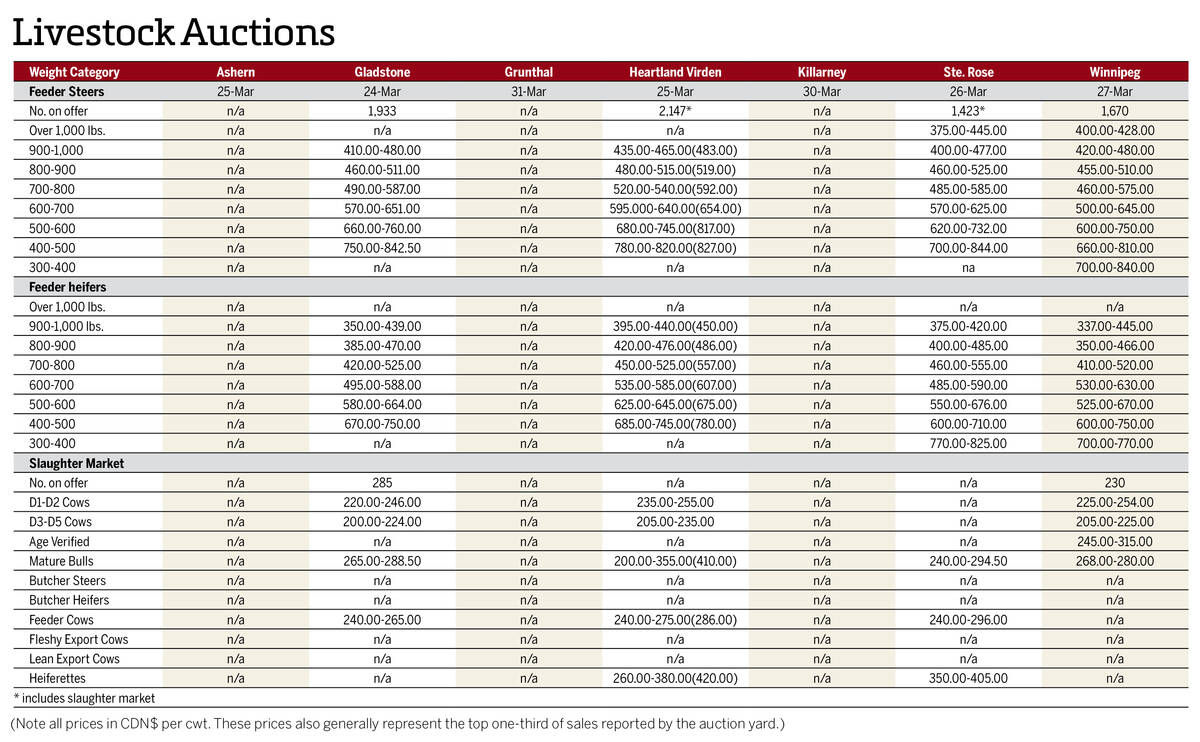

Manitoba cattle prices April 1

Here’s what cattle were selling for in Manitoba from March 24-31, 2026. Four of the seven main livestock auction marts held sales.

Total canola exports through 11 months of the marketing year hit 9.1 million tonnes, which compares with 6.3 million tonnes at the same point the previous year. China was the top destination, as expected, but at 4.6 million tonnes their demand was steady with the 4.5 million tonnes reported through June of the previous marketing year.

China’s demand in 2025/26 remains unclear given their stiff tariffs on canola oil and meal and the ever-present threat of trade action against canola seed.

While China may be a wildcard, the increased canola exports in 2024/25 were spread out to several countries. Notably, Japanese demand was nearly doubled on the year at 1.6 million tonnes, while Mexican business increased to 811,600 tonnes from 548,000.

European countries imported 1.2 million tonnes of Canadian canola from August through June, roughly 11 times the 103,000 tonnes sent during the same time the previous year.

Europe’s rapeseed production was down sharply in 2024, accounting for the increased need for imports. However, expectations are for a larger European crop in 2025, which should limit that buying interest. The U.S. Department of Agriculture is forecasting European rapeseed production at 19.5 million tonnes, which would be up from 16.9 million in 2024. As a result, they also expect European imports to fall to 5.7 million tonnes from 7.0 million.

The USDA is forecasting Canadian canola exports in 2025/26 at 7.6 million tonnes — well short of their 2024/25 target of 9.2 million.

Carry-in canola supplies for the new marketing year should be very tight, as Statistics Canada has already had to upwardly revise last year’s production numbers to make the numbers work. The first official estimates on the new crop will be released at the end of August, but early estimates see production down by at least a million tonnes or more. What a decline in both supplies and demand will mean for prices remains to be seen, but any shift in that balance will be a key driver in the months ahead.