The ICE Futures canola market has seen some wide price swings to start the new year, hitting contract highs then falling $80 per tonne off of those highs in the front month before eventually rebounding to be right back around where they started the year (as of Jan. 20).

Such large swings are to be expected, given the high price levels, with the underlying fundamentals still thought to be supportive despite the occasional bout of profit-taking.

With the nearby March contract trading around the $1,000-per-tonne level, an $80-per-tonne drop works out to an adjustment of eight per cent. While sizable, today’s $80 move is yesterday’s much-smaller $40 correction, as an eight per cent move with canola at levels closer to $500 per tonne would only be $40.

Read Also

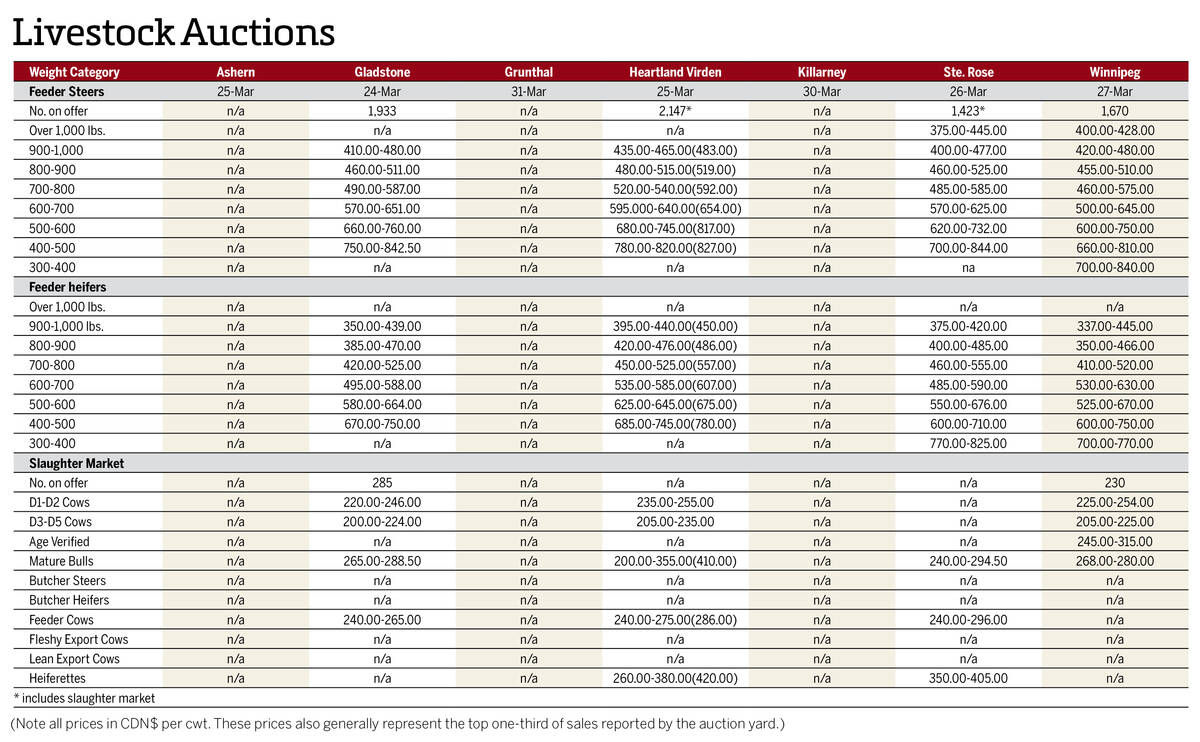

Manitoba cattle prices April 1

Here’s what cattle were selling for in Manitoba from March 24-31, 2026. Four of the seven main livestock auction marts held sales.

A general feeling shared by many traders is that large price moves will remain the order of the day in the current marketing reality, with speculators moving their money around and booking profits on both the short and long sides. However, while the highs may be in for the time being, another consensus is that the general trend remains strong.

Canada’s tight supply situation is well known and will likely remain supportive into the next crop year, as even a return to normal production in 2022 would still leave stocks on the low side. Export demand has been curtailed considerably, but the domestic crush is solid and processors continue to indicate that they need supplies.

Yet another new canola-crushing development was announced during the week — this time a 1.1-million-tonne joint-venture project between AGT Foods and Federated Co-op. The Regina-based plant is intended to provide canola oil for renewable diesel, with a fair bit of investment going into that sector over the next few years.

The new plants still need to be built, with trade in the more immediate future focused on South American weather, world energy markets and broad strength in vegetable oils.

Farmers in northern Brazil’s growing regions are just getting started with their harvests, while crops in Argentina still have a long growing season ahead of them. Heat and dryness in both countries have cut into production prospects lately, although much-needed rains were alleviating those concerns to some extent.

A little further afield, palm oil prices climbed to record highs during the week. Labour shortages and floods in some key growing regions were behind much of the strength in that market, with moves by Indonesia that could limit exports also supportive.

Turning to grains, wheat has also seen some choppiness to start the year, but recovered from nearby lows over the past week amid mounting geopolitical tensions between Ukraine and Russia. Both countries are major players in the world wheat market, and the possibility of unrest there was keeping the grain markets on edge.