Harvest operations are wrapping up across the Prairies and attention in grain markets is turning to outside influences.

Exports

Canadian canola exports were running at a solid pace through the first 10 weeks of the 2023-24 marketing year, but that pace will be hard to maintain. Production was down on the year and more of the crop will likely end up in the domestic crushing sector.

Read Also

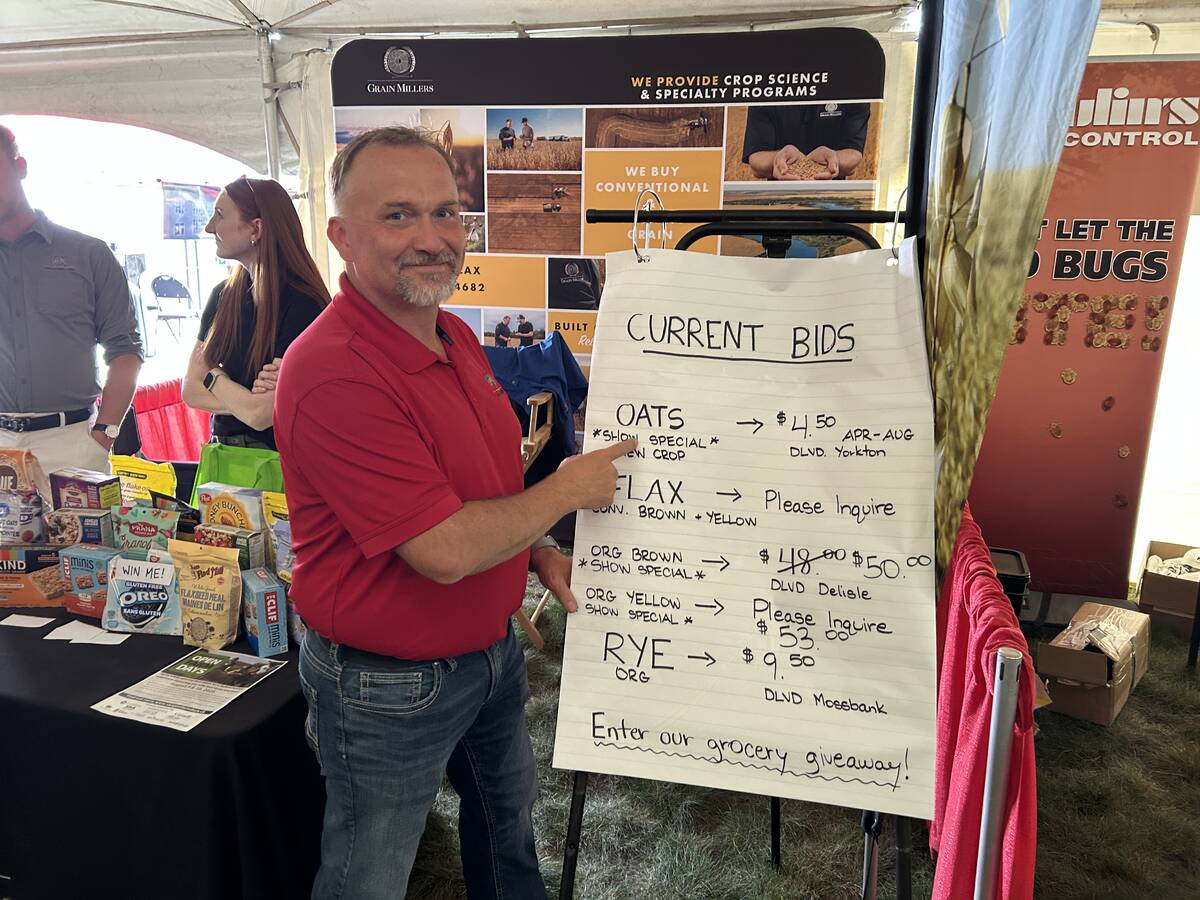

Canada’s oat crop looks promising

Oat market demand is strong. At the same time, Canada’s planted oat area is up an estimated 2.6 per cent from last year and 2025 yields may be up 2.8 bushels to the acre.

Canada exported 872,900 tonnes of canola through the first 10 weeks of the marketing year, up by about 150,000 tonnes from the same point the previous year. Domestic usage, 1.8 million tonnes, was up by 200,000 tonnes on the year, according to Canadian Grain Commission data. Discounted Ukrainian rapeseed is reportedly making its way into Europe, limiting the potential for Canadian movement. Cheaper sunflower seed oil is also tempering some demand.

Israel/Hamas

While the Gaza conflict does not have the same direct influence on grain markets as the situation in Ukraine, any unrest in the Middle East can have a sizeable impact on world energy and financial markets, especially if Iran or other countries were to become more directly involved.

Crude oil saw big price swings in the aftermath of the Hamas attacks and Israeli response, but where things shake out from a marketing standpoint remains to be seen.

Ukraine/Russia

While the ongoing war has been pushed off the front pages for now, grain movement out of both countries is still being followed closely by the agricultural markets.

Ukraine released export data during the week showing a sharp decline in export volumes this year compared to a year ago, as Russian blockades in the Black Sea slow movement. Meanwhile, Russian President Vladimir Putin told a meeting of the Commonwealth of Independent States that Russia will have total grain exports of 50-60 million tonnes.

The U.S. Department of Agriculture upped its forecast for Russian wheat exports in 2023-24 to 50 million tonnes, from an earlier estimate of 49 million, and expects Ukrainian wheat exports of 11 million tonnes. If realized, Ukrainian exports would be well below the 17.1 million tonnes moved the previous year, while the Russian movement would be up by 2.5 million tonnes.

Canadian wheat exports are running at a solid pace through the first 10 weeks of the 2023-24 marketing year at 3.8 million tonnes to date. That compares with 3.3 million at the same point the previous year.

USDA forecasts total Canadian wheat exports at 23 million tonnes, which would be up from Agriculture and Agri-Food Canada’s current estimate of 21.5 million tonnes, but below the 25.5 million tonnes moved the previous year.