The ICE Futures canola market started the new year much the same as it ended the old, trending higher in an ongoing effort to ration demand in the face of tight supplies. That underlying sentiment should remain a supportive influence over the next few months, although outside influences do have the potential to trigger short-covering corrections from time to time.

Nearby canola futures were all trading above the psychological $1,000-per-tonne level to start 2022, with new-crop prices nearing $800 per tonne, historically strong in their own right.

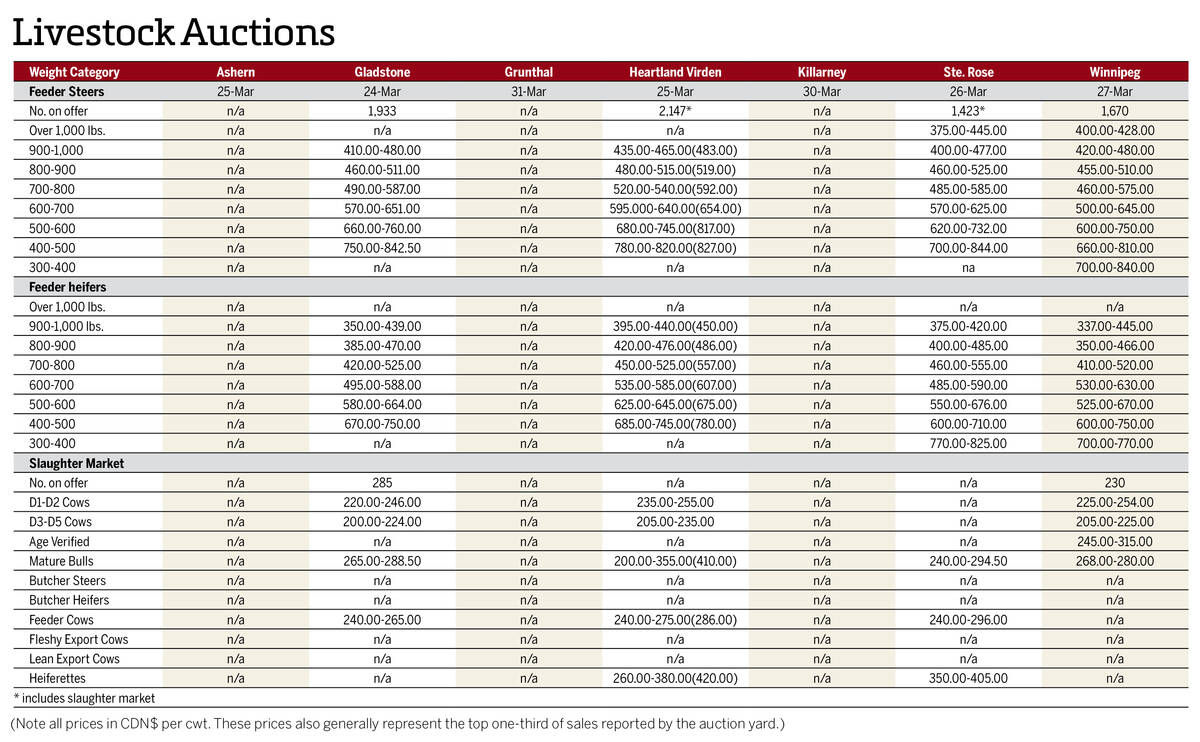

Read Also

Manitoba cattle prices April 1

Here’s what cattle were selling for in Manitoba from March 24-31, 2026. Four of the seven main livestock auction marts held sales.

With prices as high as they are, the inevitable corrections could be severe while maintaining the general bullish uptrend. Looking at the March contract trading at $1,030 on Jan. 7, it could lose $20 per tonne in a day and still be above its 20-day moving average. It would take a $100 drop to test the 100-day average, while chart indicators that would indicate an overbought market all remain safely in the neutral zone.

The canola supply situation will remain tight until next summer at the earliest, and even then it will take a massive crop to restock to pre-drought levels. Domestic processors want to ensure delivery so they can keep operating, while exports can be expected to be cut considerably.

The latest data from the Canadian Grain Commission highlights that processor demand, with domestic usage to date of about four million tonnes only off by half a million from the previous year. Meanwhile, the 2.9 million tonnes of canola exported through the first 22 weeks of the 2021-22 crop year are well off the 5.2 million moved at the same time a year ago. Export movement is expected to fall off even more in the next few months, with maybe only one million to 1.5 million tonnes left to move.

Looking to the south, the soybean and corn markets in the U.S. have their sights set firmly even farther south, on the crops in Brazil and Argentina. Forecasts calling for hot and dry weather in some key growing areas provided a bit of a boost to those markets during the week, with excessive moisture in northern Brazil also lending support to soybeans. However, export movement has been soft lately and total world supplies of the two crops are still expected to be more than sufficient to meet demand.

Meanwhile, wheat has been in free-fall mode in recent weeks, posting large losses as speculative profit-taking and expectations for large crops in the Southern Hemisphere weighed on values. The losses in wheat came despite declining crop ratings for winter wheat in the U.S. and Canada’s tight supply situation. Tensions in Russia, Ukraine, and now Kazakhstan were also being followed closely by wheat traders to start the year.