A question I get asked a lot is, “Where are canola prices going?”

That’s not something you can answer just by looking out your back door, throughout your province, or even across the Prairies. You really have to look around the world at all oilseed markets to get a better sense of where our canola prices could go.

So many factors worldwide combine to affect prices. From production science, to consumer trends, to shipping and logistics, from new product uses, government regulations and trade barriers, to commodity substitutability — all affect the marginal supply and demand of that last ounce of a commodity. And, it’s at that last marginal amount where prices get determined.

Read Also

Flea beetle control goes outside the box at Ag in Motion

The stops at the 2025 Ag in Motion farm show feature an entomologist experimenting with trap crops and marigolds as concepts to control flea beetles.

Given all these factors, how much is someone willing to pay for that last bushel compared to the next bushel? Any and all of these factors can be an issue. But in the markets, something isn’t an issue until it becomes an issue, and then it can be a real issue.

In the big picture, while canola is a major crop in Canada, global canola/rapeseed oil production is only about 50 per cent of soybean oil production and 40 per cent of palm oil production worldwide. When you combine all the top 10 largest oils like sunflower, palm, peanut and coconut, rapeseed oil production worldwide is about 15 per cent of the global edible oil market.

While Canada is the second-largest canola/rapeseed producer, it only represents about 25 per cent of global production. Even though production and growing condition across the Prairies will affect potential canola supply and therefore domestic prices, external global production and price influences can often offset these domestic factors, unless weather conditions here are really extreme. At the end of the day, our canola represents around five per cent of this global consumable oil market, based on USDA figures.

Finally, given Canada exports 90 per cent of its canola as seed, oil or meal to 50 markets around the world, domestic consumption doesn’t have much impact on our canola prices.

So, again, you really do need to look around the world to get a sense of other oilseed factors impacting our prices here at home.

To start, let’s look at a close competitor to us both in terms of product substitutability and proximity: the U.S. soybean market. The size alone of U.S. soybean production means it will have an impact on our canola prices. U.S. soybean production of about 120 million tonnes is about six times the 20 million tonnes of Canadian canola production.

Based on price charts in equivalent U.S. dollars, you can certainly see this influence: where soybean oil futures go, canola futures tend to move in the same general direction.

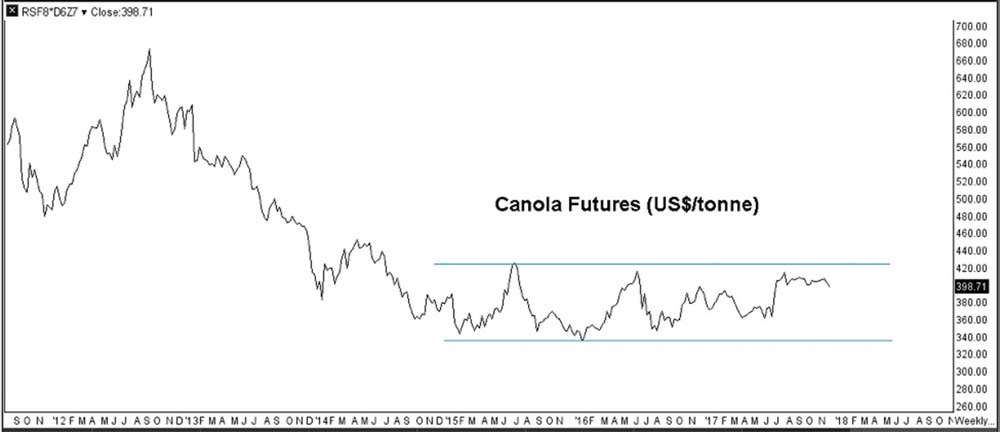

The same is true of the European rapeseed market. Europe produces about 22 million tonnes of rapeseed and is the world’s biggest producer of rapeseed oil at over 10 million tonnes. The European rapeseed oil price has been in a channel chart pattern for the past several years.

In fact, all the largest oil markets including soybean, rapeseed, palm and sunflower have a similar price pattern. All these global oilseed markets have been going sideways over the past couple of years, so expect more sideways canola price action until a definitive change in oilseed trends occur. Where they go, canola will tend to follow.

Sometimes it also helps to look at what forward prices curves are doing to get a sense of underlying market fundamentals. Futures curves for canola, soybean and soyoil are all relatively flat or slightly upward sloping, suggesting that there aren’t any particular imbalances in current market conditions. Once again, sideways prices can be expected, for now.

Finally, with oilseed production and consumption so global in nature, currencies will also affect our canola prices. A look at the Canadian dollar can also help answer the canola price question. Interestingly, the Canadian dollar too looks very similar to all these other charts: basically choppy for the past three years.

Bottom line, until we get some evidence that this directionless trend has ended, expect canola prices to continue to go sideways. However, canola prices often move up or down $50/tonne in any given three-month period. A $50/tonne swing can easily occur even as canola stays within its longer-term technical sideways price pattern around $500/tonne.

Use flexible options and futures strategies to take advantage of any price rallies while being prepared to protect revenues against a breakdown in prices. In conjunction with cash sales, deferred delivery and basis contracts you may already use, options and futures give you the extra downside price protection you need but with the upside potential you want.

So remember, in our world of interrelated markets, think globally about what’s going on around the global oilseed market, but act locally to protect revenues, manage risk and take advantage of pricing opportunities.