After nine straight days of declines, the ICE Futures canola market finally saw a splash of green the day before St. Patrick’s Day.

The most active May contract hit a session high of $829.50 per tonne on March 3, then proceeded to lose roughly $90 over the next two weeks. It hit a low of $737.20 on March 16. That’s where some buying finally materialized and the contract managed to settle well off that level at $755.80 per tonne.

Damage was done from a chart standpoint by the slide and more losses are possible, but there are also enough supportive influences to indicate the market may be headed into a corrective period.

Read Also

Manitoba cattle prices April 1

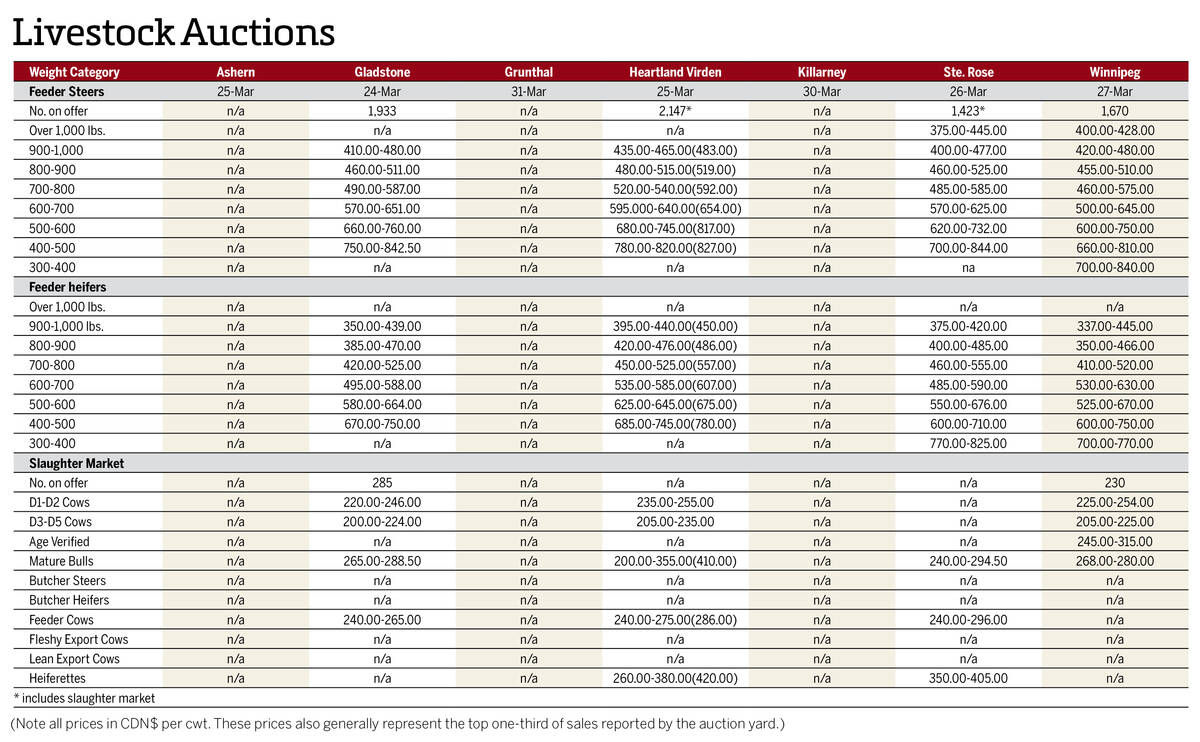

Here’s what cattle were selling for in Manitoba from March 24-31, 2026. Four of the seven main livestock auction marts held sales.

Weekly Commitments of Traders data from the U.S. Commodity Futures Trading Commission was getting back up to speed after technical issues delayed reports for most of February, but the large net managed-money short position of 46,222 contracts as of March 7, in combination with near-record open interest in the canola market, would be a key sign that speculators were happy with the price drop and likely adding to their shorts to boost profits.

Eventually they’ll want to come back to the buy side and cover those positions, which would be supportive in the long run.

Several of the technical indicators those speculative traders like to track were looking heavily overdone, while wide crush margins remain bullish from a fundamental standpoint.

Crush margins of $250 per tonne or more above the futures compare to the same time a year ago, when domestic processors were barely breaking even, according to the official numbers. The domestic crush is running at close to full capacity. The 6.6 million tonnes of canola crushed through the first 32 weeks of the 2022-23 crop year are well ahead of the previous year’s pace.

Exports of 6.5 million tonnes to date are also up on the year, according to Canadian Grain Commission data. However, a record-large Australian crop is expected to cut into that movement, while losses in European rapeseed values were also making Canadian canola look more expensive on the global market.

As a result, there are ideas that export movement may slow down in the months ahead.

Another factor to watch is the price spread between canola and soybeans. Canola typically trades at a premium of about $50 per tonne above soybeans, but values moved close to par as soybeans did not fall to the same extent as the Canadian oilseed.

Soybeans have been propped up by production uncertainty in Argentina, but those drought issues are well known by now, so the spread will likely ease into more traditional territory. Whether that means higher canola, lower soybeans or a combination of the two remains to be seen.

Farther afield, markets have their eyes on North American weather conditions, as seeding operations get underway in the southern U.S. and winter wheat is already filling in Texas. The extension of the Black Sea grain deal, allowing for Ukrainian exports, will also be followed closely.