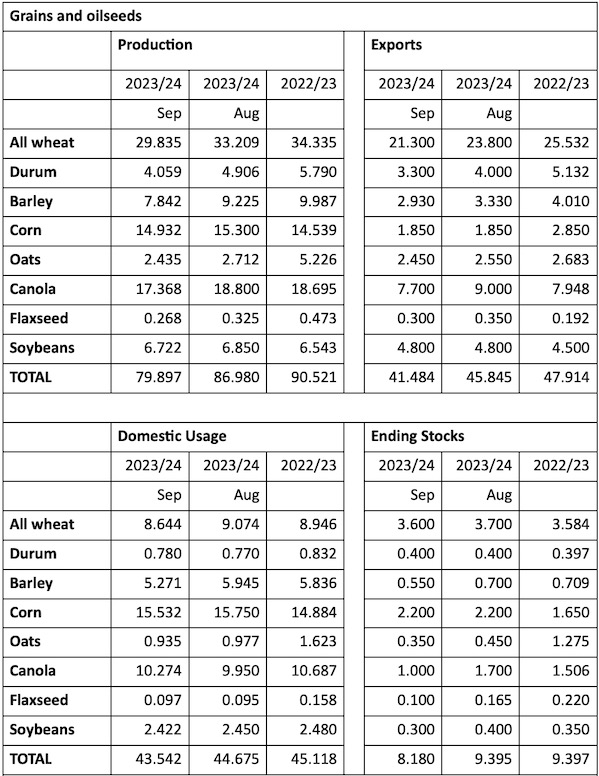

MarketsFarm –– Canadian canola carryout supplies for the current marketing year will likely end up tighter than earlier expectations, according to updated supply/demand balance sheets from Agriculture and Agri-Food Canada (AAFC) that account for recent production and stocks data from Statistics Canada.

Canola ending stocks for 2023-24 are now forecast to tighten to only one million tonnes, down by 700,000 from the August forecast and well below the 2022-23 canola carryout of 1.506 million tonnes.

Canola production was down from the August estimate — now at 17.368 million tonnes, which compares with the 18.695 million tonnes grown in 2022-23. Canola exports were forecast at 7.7 million tonnes, which would be well below the nine million tonnes forecast in August but in line with the 7.948 million tonnes exported in 2022-23.

Read Also

Prairie Wheat Weekly: Rising loonie pushes down cash prices

Cash prices for Western Canadian wheat and durum stepped back during the week ended March 11, pushed lower by a stronger Canadian dollar.

Meanwhile, projected domestic usage for canola in 2023-24 was raised to 10.274 million tonnes, from 9.95 million in August.

Wheat ending stocks for 2023-24 were lowered to 3.6 million tonnes by AAFC, from an estimated 3.7 million tonnes in August. Both exports and domestic usage were revised lower for wheat, but the declines in demand were more than countered by the sharp decline in production to 29.835 million tonnes from 33.209 million in August. Canada grew 34.334 million tonnes of wheat in 2022-23 and had a carryout of 3.584 million tonnes.

Total wheat exports for 2023-24 are now forecast at 21.3 million tonnes by AAFC, which was down by 2.5 million tonnes from August and compares with the 25.532 million tonnes of Canadian wheat exported the previous crop year.

Barley ending stocks for 2023-24 were forecast at 550,000 tonnes, which would be down from the August estimate of 700,000 tonnes and the 2022-23 level of 709,000 tonnes.

The carryout for oats was lowered by 100,000 tonnes, to 350,000 tonnes. If realized, that would be a drastic reduction from the 1.275 million tonnes carried forward from 2022-23.

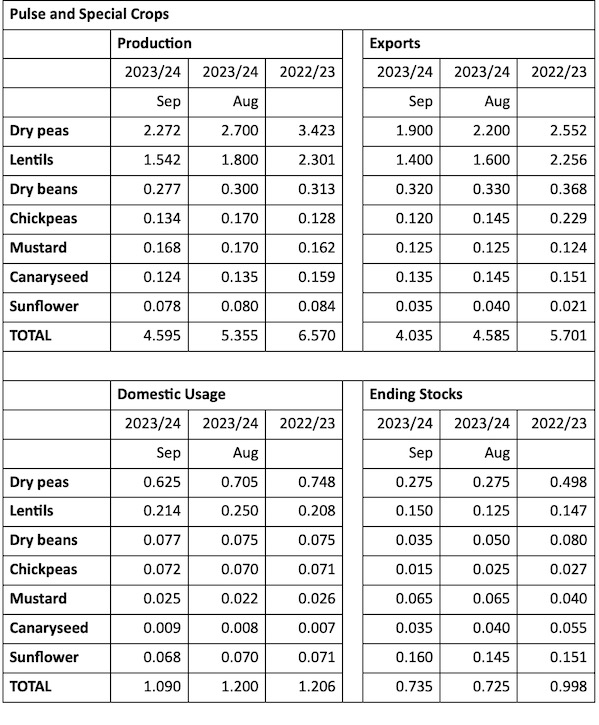

Pulse and special crops only saw minor adjustments, with projected pea ending stocks for 2023-24 left unchanged at 275,000 tonnes while lentils were upped slightly at 150,000 tonnes.

Tables: September estimates for Canadian major crops supply and demand: in millions of metric tonnes. Source: Agriculture and Agri-Food Canada.